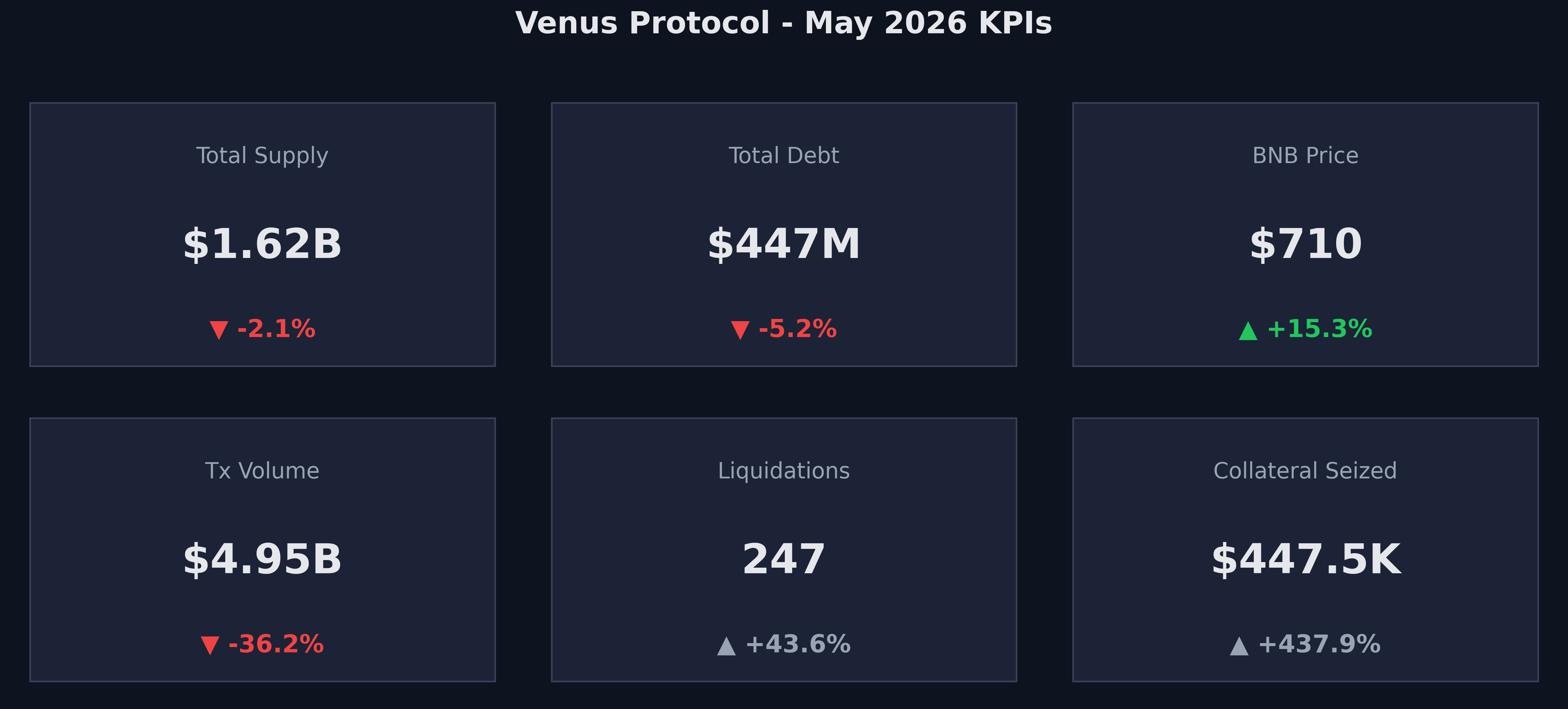

BNB rallied 15.3% across May, from $615 to $709.50, and Venus Core Pool reduced risk over the same period. Total supply edged down from $1.659B to $1.623B (-2.1%) and debt from $471.4M to $446.9M (-5.2%). The dollar decline reflects contraction in BTC, ETH, and USDC markets that outweighed the BNB-denominated mark-up, so the headline numbers understate how strong the BNB leg was. Liquidations stayed contained at $447.5K across 247 events, with no cascade. The clearest risk improvement was on ETH, where large April borrowing positions unwound and utilization fell from 88.3% to 48.4%. On governance, Venus added two new safeguards, a tighten-only EBrake Executor and the Oracle Dynamic Protection Mode, alongside the continued wind-down of a few deprecated markets. The health factor distribution stayed healthy: most low-health-factor debt is correlated E-mode leverage, leaving only $10.9M of genuinely directional Critical exposure.

1. Market Context & BNB Price

Venus Core Pool closed May 31 with:

-

Total Supply: $1.623B (-2.1%)

-

Total Debt: $446.9M (-5.2%)

-

BNB Price: $709.50 (+15.3%)

-

Transaction Volume: $4.95B (-36%)

-

Liquidations: 247 events (+43.6%)

-

Collateral Seized: $447.5K (+437.9%)

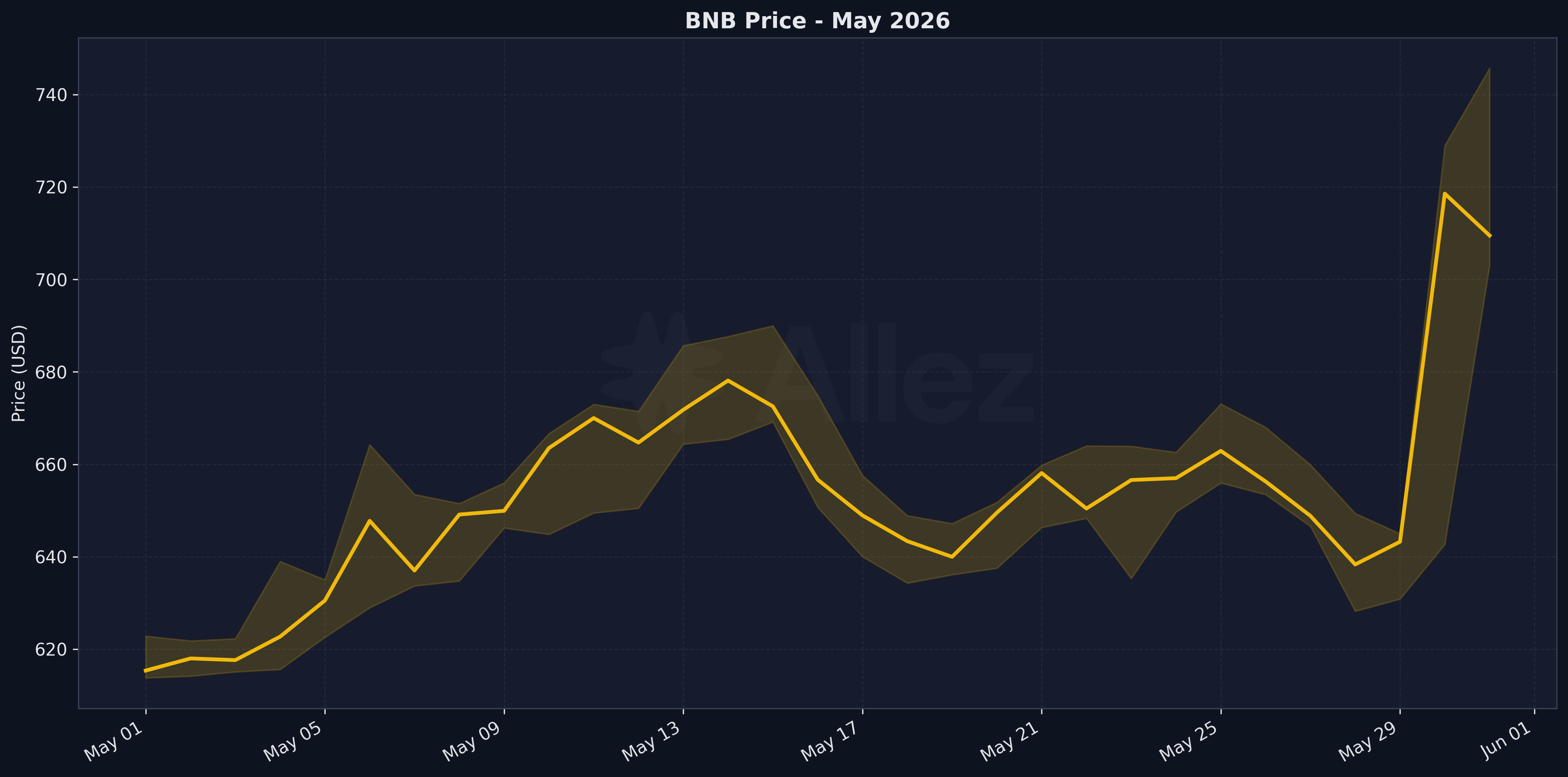

BNB opened May at $615.37 and closed at $709.50, a 15.3% gain over the April 30 close. The intra-month low was $613.79 and the high was $745.74, with most of the appreciation arriving over the final three days (May 29 to 31). For most of the month BNB traded in a $640 to $680 band, so the rally was concentrated rather than a steady climb.

The price move matters because the BNB collateral category (BNB, WBNB, asBNB, slisBNB) totals $567M, the second-largest grouping in the pool behind BTC. A 15% appreciation lifts the dollar value of that collateral and improves the health factors of BNB-collateral borrowers, which is consistent with the calm liquidation profile described in Section 4. The mirror image is that protocol-wide supply and debt fell in dollar terms despite the rally, because the BTC, ETH, and USDC markets contracted enough to offset the BNB mark-up. Token-quantity detail is covered in Section 2.

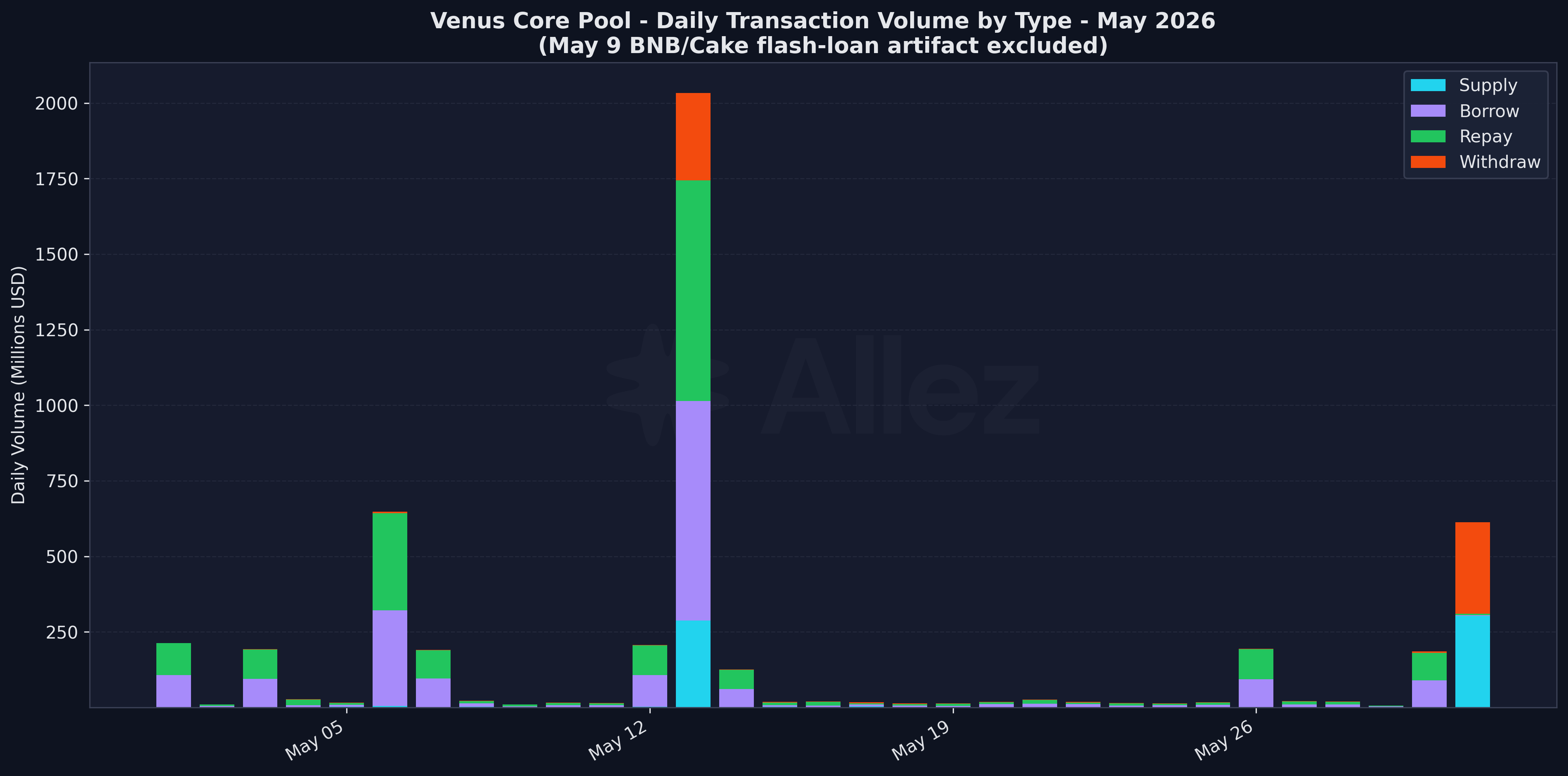

The raw transaction-volume series reported $1,360B for the month, but 99.6% of that came from a single day, May 9, where BNB supply and withdraw each posted $632B (implying 971 million BNB tokens in a single day, against a market that holds about 570,000) alongside a matched Cake borrow and repay of $45.5B. These equal, same-day, same-asset pairs are flash-loan or same-block looping activity that nets to zero, not economic flow, and have been excluded. The clean monthly volume is $4.95B, in line with the normal $5-6B range.

Venus Ecosystem Updates:

-

vSXP market deprecation executed. Chainlink retired the SXP/USD price feed on May 11, 2026, the sole oracle for the vSXP market. After that date the market became unpriceable and supply/repay were no longer possible. Residual exposure was negligible ($342 supplied). SXP no longer appears in the month-end market snapshot. (forum notice)

-

DAI off-boarded as collateral. DAI's collateral factor was reduced to 0% as part of the May risk-parameter update, citing Sky Protocol's DAI to USDS migration which has put DAI in effective deprecation. Existing positions are unaffected. The change caps new borrowing against DAI. (proposal)

-

Wk20 VIP (mid-May) bundled the TUSD and FIL wind-down, activation of the tighten-only EBrake Executor (audited by CertiK and Hashdit), and a marketing-funding transfer. (VIP)

-

Oracle Dynamic Protection Mode (mid-May). This Venus proposal deploys a DeviationBoundedOracle that wraps the existing Resilient Oracle with a per-market rolling 15-minute min/max price window, returning a bounded price on the borrow path when spot deviates beyond the per-market threshold. It hardens the borrow path against price-manipulation and flash-volatility risk. (proposal)

-

Venus Prime redesign put to a Snapshot vote (May 26), proposing more rewards, monthly competitions, and open access to the Prime program. The vote was in progress at month-end. (post)

-

Venus Trade launched on BNB Chain (teased early May, around May 6), a relative-performance trading product that opens a long/short pair in a single position (for example, long BNB and short ETH), built on the lending infrastructure with self-custody, partial liquidations, and continuous yield. (thread)

2. Supply & Market Overview

Top markets by supply (May 31):

| Market | Supply | MoM | Debt | Util |

|---|---|---|---|---|

| BNB | $404M | +13.2% | $116M | 28.7% |

| BTCB | $393M | -12.1% | $121M | 30.8% |

| USDT | $205M | -7.3% | $119M | 57.9% |

| SolvBTC | $185M | +4.3% | $1M | 0.3% |

| asBNB | $92M | +12.4% | $0M | 0.0% |

| WBNB | $69M | +15.6% | $12M | 16.8% |

| xSolvBTC | $55M | -10.9% | $0M | 0.0% |

| USDC | $51M | -31.7% | $32M | 62.9% |

| ETH | $40M | -10.9% | $20M | 48.4% |

| U | $29M | +8.8% | $12M | 42.7% |

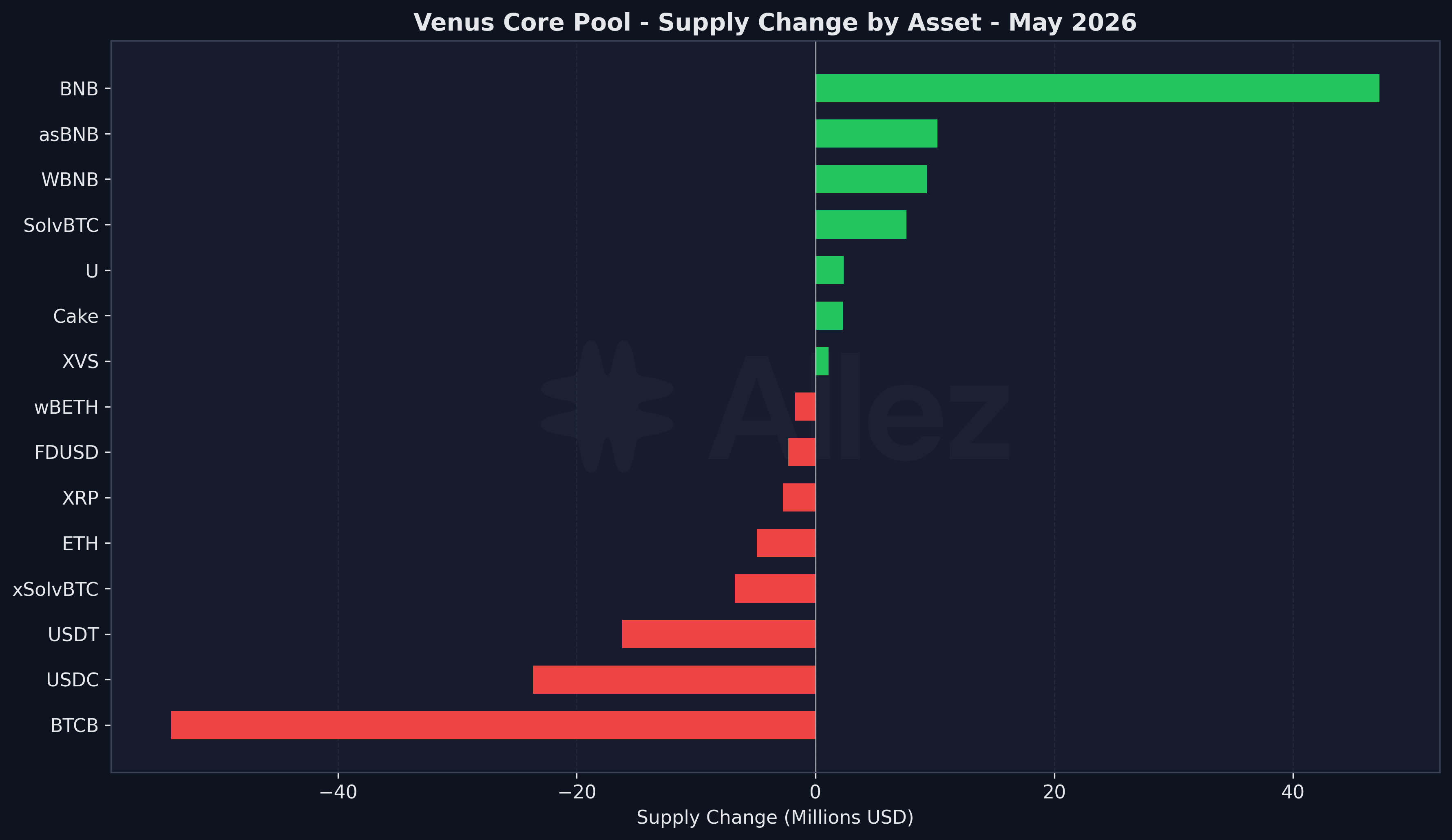

Several large moves in the table are mark-to-market, not real flow. With BNB up 15.6% over the snapshot window, BNB supply rose 13.2% in dollars but fell 2.0% in token terms (580,688 to 568,855 BNB), so the apparent growth is the price rally net of a small token outflow. WBNB tells the same story (up 15.6% in dollars, flat at 97,300 tokens), and asBNB grew 12.4% in dollars while declining 2.8% in tokens.

BTCB moved the other way. Its dollar supply fell 12.1%, and because BTC declined only 3.0% over the window, most of that is a real token outflow: BTCB holdings dropped from 5,869 to 5,322 tokens (-9.3%). xSolvBTC saw a similar token decline (-8.3%), while SolvBTC (a BTC-backed token from Solv Protocol) bucked the trend with a 7.4% token inflow (2,318 to 2,489), lifting its dollar supply 4.3%. ETH supply fell 10.9% in dollars but its token quantity held flat (-0.3%), so the decline there is purely the 10.7% ETH price drop rather than withdrawals.

USDC drove the largest real outflow: supply fell 31.7% ($74.6M to $50.9M) and debt fell 21.3%, a stablecoin-side contraction unrelated to price. U, a smaller dollar stablecoin, was the only stablecoin gainer, with debt up 57.5% off a small base, though still immaterial at $12M against a $210M cap.

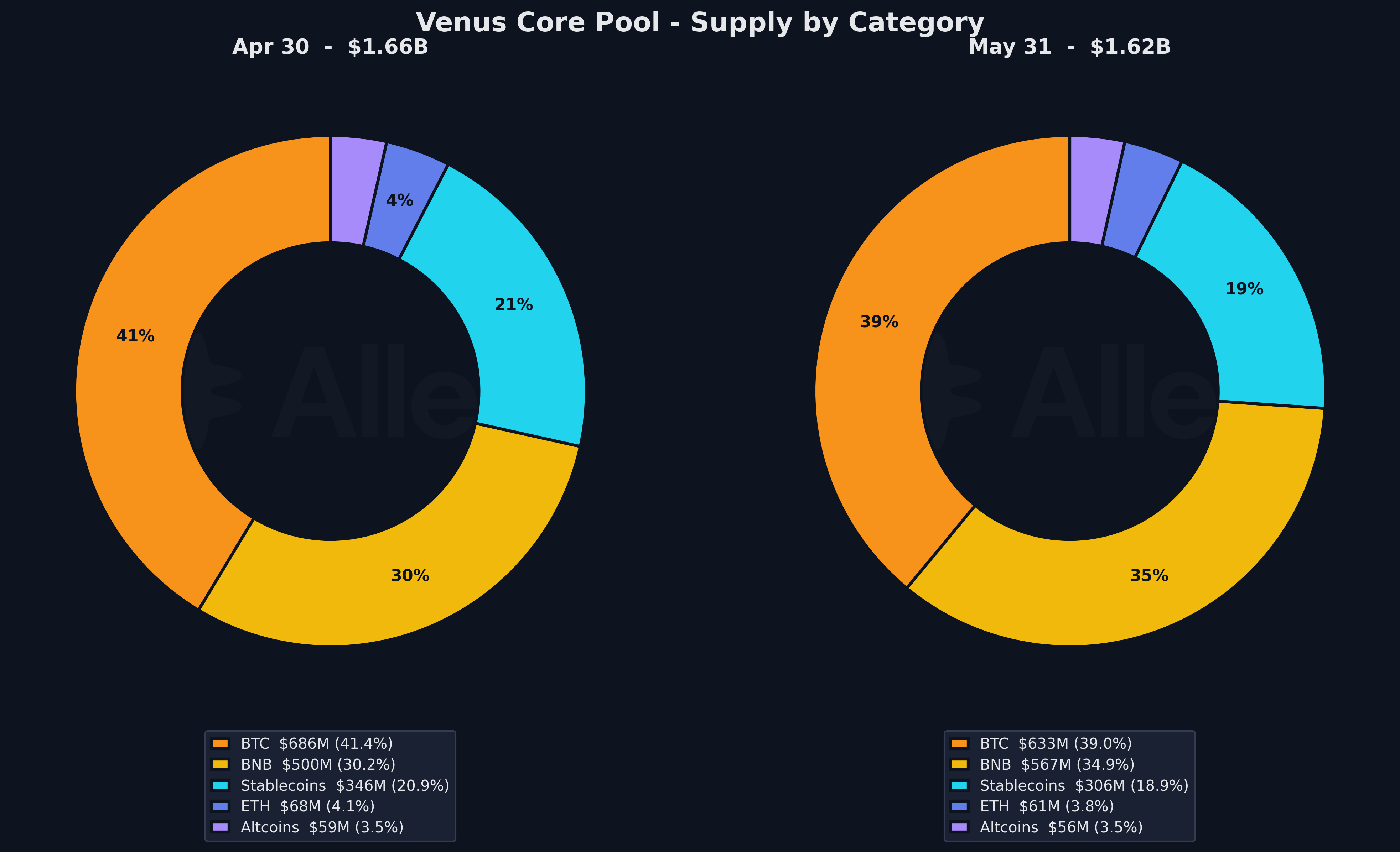

Category composition (May 31):

| Category | Supply | Share | MoM (pp) | Debt |

|---|---|---|---|---|

| BTC | $633M | 39.0% | -2.4 | $122M |

| BNB | $567M | 34.9% | +4.8 | $128M |

| Stablecoins | $306M | 18.9% | -2.0 | $176M |

| ETH | $61M | 3.8% | -0.3 | $20M |

| Altcoins | $56M | 3.5% | -0.1 | $2M |

The composition shift is driven almost entirely by the BNB rally. BNB's share rose nearly 5 percentage points to 34.9%, closing much of the gap with BTC, which slipped to 39.0% as BTCB holders withdrew tokens into a softer BTC price. Stablecoins gave back 2 percentage points to 18.9%, led by the USDC outflow and the DAI off-boarding. ETH and Altcoins together hold under 8% of supply and barely moved. Wind-down assets continue to bleed at zero collateral factor: FIL among the altcoins, and DAI and TUSD on the stablecoin side.

On a daily basis, protocol supply drifted from $1.677B at the start of the month to $1.623B at month-end, tracking the BTC and USDC contraction through mid-month before the late BNB rally lifted the BNB leg. The largest single-day move was a $64M supply increase on May 30 as the BNB rally accelerated, with no abrupt shocks.

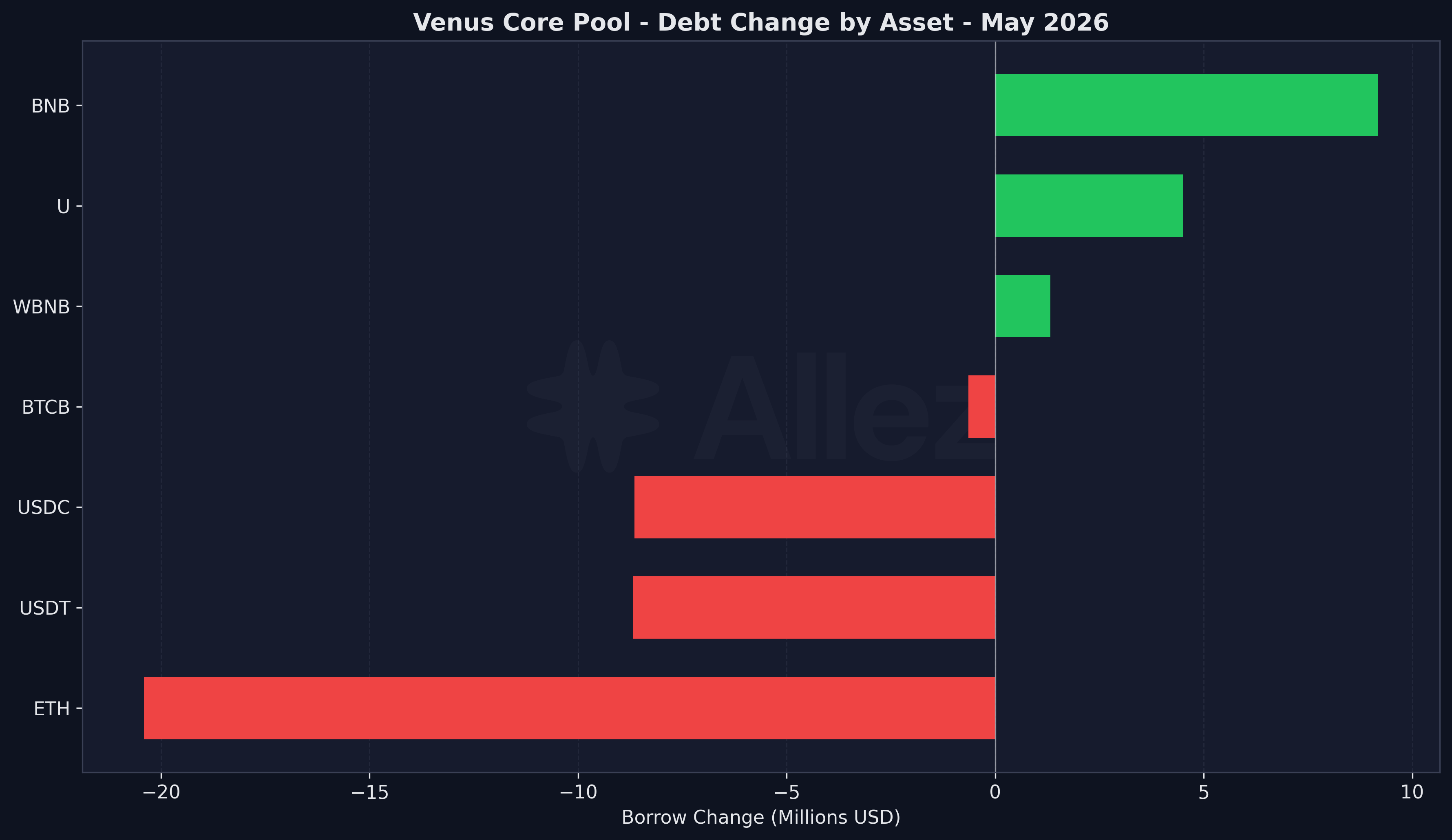

The dollar-change view shows BNB, WBNB, and asBNB as the top inflows (price-led) and BTCB and USDC as the largest outflows (token-led). The debt-change view (chart 06b) is dominated by the ETH unwind discussed in Section 7.

Note: Per-asset figures reflect token quantity changes valued at current prices, isolating user deposit and withdrawal behavior from price effects.

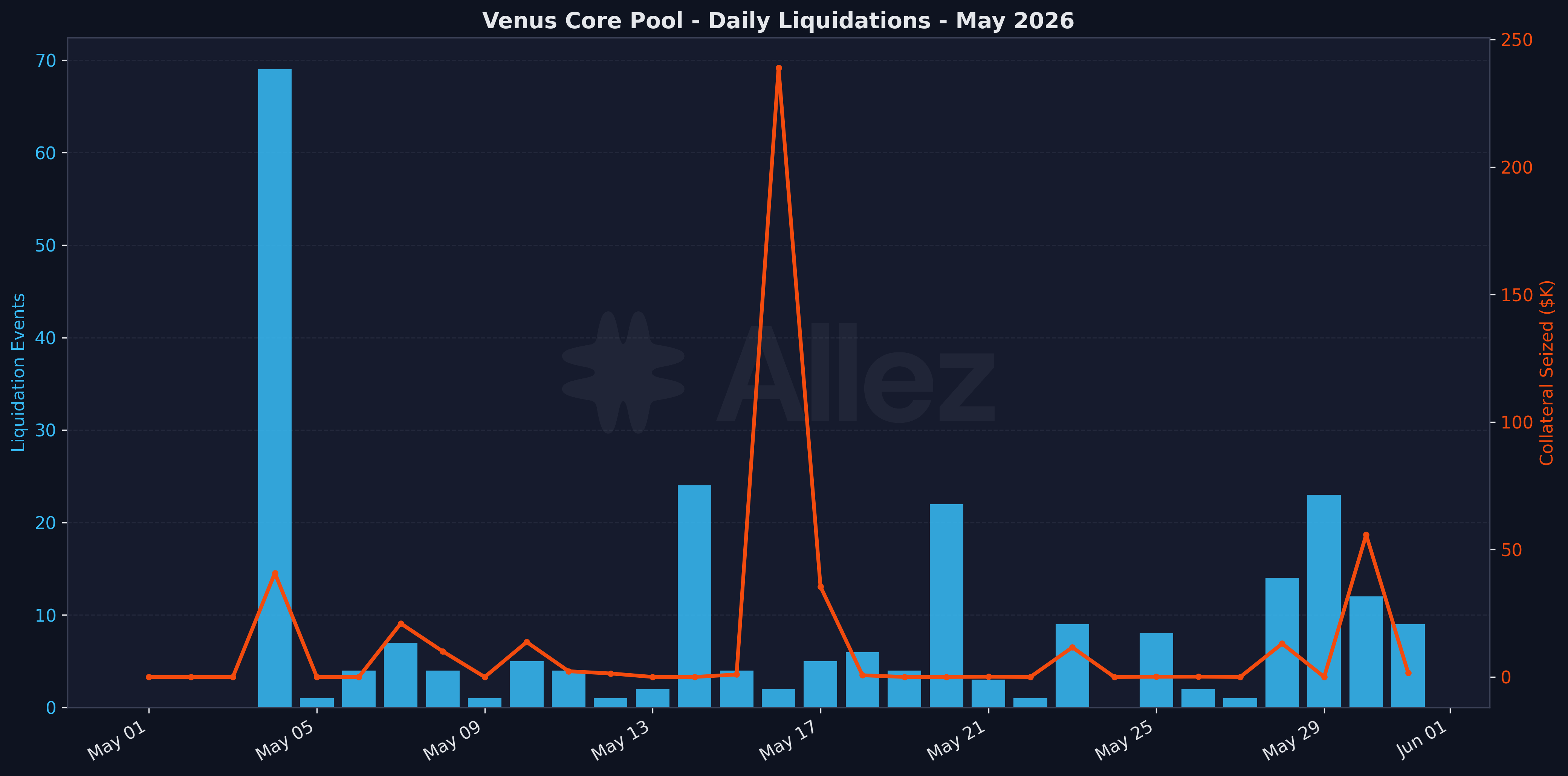

3. Risk & Liquidations

Liquidation summary:

| Metric | May Total |

|---|---|

| Total events | 247 |

| Collateral seized | $447.5K |

| Peak seized day | May 16 ($238.8K) |

| Peak event-count day | May 4 (69 events) |

The 247 events seized $447.5K with no cascade, well short of a stress month where seizures run into the tens of millions and chain across markets. Two patterns stand out. May 4 to 5 produced the largest count of small liquidations (69 events on May 4), and the $238.8K seized on May 16 was a single liquidation of an ETH-collateral position against stablecoin debt, consistent with mid-month ETH softness rather than a broad sweep. The increase from April's $83.2K reflects the ETH drawdown catching a few larger positions, not a systemic event.

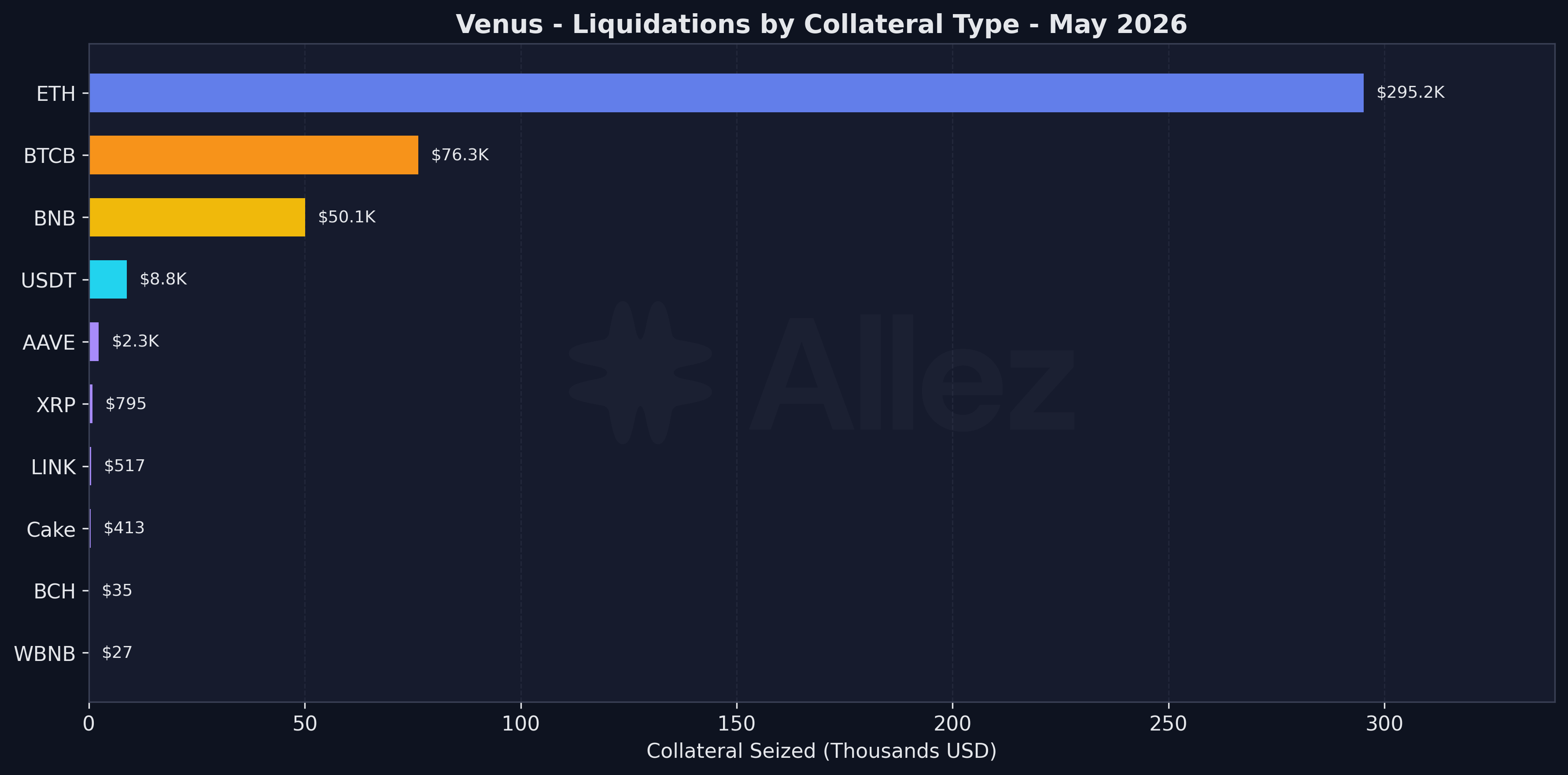

Top collateral by seized value:

| Collateral | Seized | Events |

|---|---|---|

| ETH | $295.2K | 32 |

| BTCB | $76.3K | 33 |

| BNB | $50.1K | 34 |

| USDT | $8.8K | 45 |

| AAVE | $2.3K | 11 |

ETH collateral accounted for $295.2K, two-thirds of all seized value, consistent with ETH being the weakest major collateral (-10.7%) and the May 16 spike. The events themselves stayed small and spread across markets, with no single market producing a stress-level liquidation.

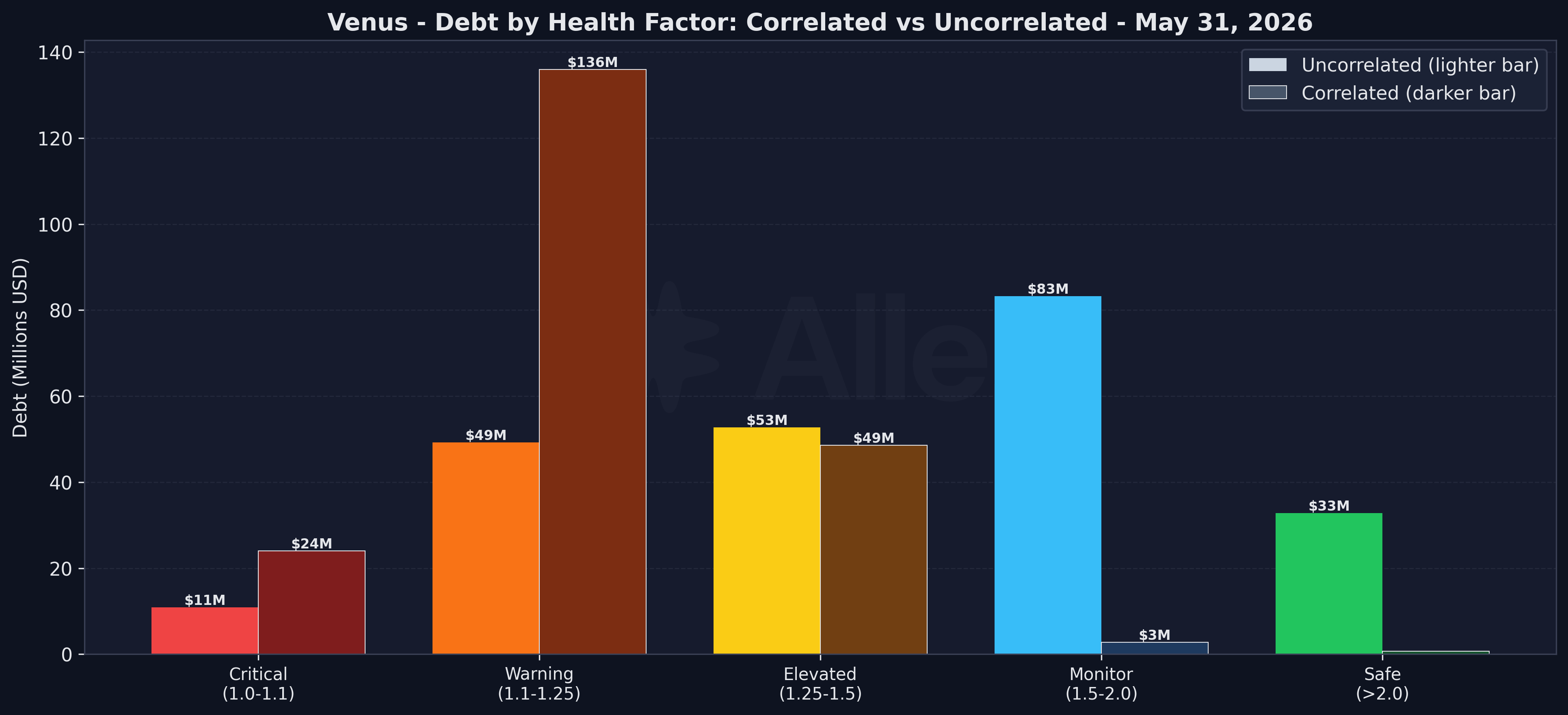

Health factor distribution (May 31):

Splitting each health-factor band into correlated and uncorrelated debt separates structural leverage from directional risk. Correlated debt (E-mode loops like SolvBTC against BTCB or asBNB against BNB) carries de-peg and redemption risk rather than directional price risk: at a health factor near 1.1, a sub-1% break in a wrapper or LST peg is enough to liquidate. Uncorrelated debt (BNB or stablecoins borrowed against unrelated collateral) carries the directional risk.

| Tier | Correlated Debt | MoM | Corr. Pos. | Uncorrelated Debt | MoM | Uncorr. Pos. |

|---|---|---|---|---|---|---|

| Critical (1.0-1.1) | $24.0M | +8.1% | 96 | $10.9M | -32.3% | 51 |

| Warning (1.1-1.25) | $136.0M | +54.7% | 216 | $49.2M | +37.0% | 367 |

| Elevated (1.25-1.5) | $48.6M | -52.7% | 141 | $52.8M | +1.9% | 709 |

| Monitor (1.5-2.0) | $2.8M | -3.4% | 61 | $83.3M | -22.5% | 812 |

| Safe (>2.0) | $0.7M | +16.7% | 91 | $32.8M | -14.6% | 1,176 |

The Warning band (1.1-1.25) is the largest, holding $185.2M of debt, 42% of the borrower total and up 49.6% from April against a matching $53M decline in the Elevated band. That migration is almost entirely on the correlated side (+54.7% MoM): a block of E-mode positions whose health factors compressed from the 1.25-1.5 range into 1.1-1.25 over the month. Because both legs of an E-mode position track the same asset, this is structural leverage rather than a build-up of directional risk, and the $136.0M sits in just 216 large positions rather than across thousands of smaller retail borrowers.

The Critical band (1.0-1.1) holds $34.9M, 7.9% of borrower debt and down 8.6% from April. Of that, $24.0M is correlated and therefore low gap risk: E-mode borrowers (SolvBTC/BTCB, asBNB/BNB) whose health factor sits near 1.1 by design because both sides track the same asset. The genuinely directional Critical exposure is the $10.9M uncorrelated bucket across 51 positions, down from $16.1M in April, a 32% reduction in directional Critical risk. That improvement is partly offset one tier up: uncorrelated Warning-band debt grew 37% to $49.2M. Total directional debt fell 8% over the month, but the slice within 25% of liquidation (Critical plus Warning) rose from $52.0M to $60.1M as positions migrated down from the Monitor and Safe bands. The directional book got smaller but sits closer to the boundary.

Stablecoin debt by collateral:

| Collateral | Stablecoin Debt | Within 10% of Liquidation |

|---|---|---|

| BTCB | $73.3M | $3.5M |

| SolvBTC | $34.5M | $0.0M |

| BNB | $28.3M | $0.1M |

| ETH | $9.0M | $0.2M |

| USDT | $7.9M | $5.5M |

| wBETH | $6.8M | $4.3M |

Stablecoin debt against volatile collateral is where directional risk concentrates, and only $13.5M of it sits within 10% of liquidation. BTCB backs $73.3M with just $3.5M near its threshold and SolvBTC backs $34.5M with essentially none. The two exceptions are wBETH ($4.3M of $6.8M near liquidation, the position most exposed to a further ETH decline) and USDT collateral ($5.5M of $7.9M): the high near-liquidation share there reflects tightly-levered stablecoin loops that are calm day to day but would cluster at liquidation in a de-peg.

Borrower concentration:

The five largest borrowers carry $148M of debt, 35% of the protocol total, with the top three at $117M (28%). Figures are a recent position snapshot, with shares taken against total protocol debt of $420M at that snapshot.

| Borrower | Debt | Collateral | HF | Position type |

|---|---|---|---|---|

0x3e87…d90c | $49.8M BNB | $85.5M (asBNB-led, mixed) | 1.26 | Mostly correlated (asBNB against BNB) |

0xc482…82a8 | $40.4M BTCB | $60.4M (SolvBTC, xSolvBTC) | 1.26 | Correlated (BTC E-mode) |

0x5c18…fe77 | $27.1M BNB | $39.5M (BTCB, USDT) | 1.16 | Directional (BNB vs BTC and stables) |

0x9614…8bf1 | $18.2M (BTCB, USDT) | $24.7M BTCB | 1.09 | Mostly correlated (BTCB self-loop) |

0xaf9b…801e | $12.1M BTCB | $17.6M (SolvBTC, xSolvBTC) | 1.22 | Correlated (BTC E-mode) |

Four of the five run correlated or E-mode structures, so their tight health factors (1.09 to 1.26) are structural and unwind within the same asset family at low market impact. The third-largest is the exception and runs the other way: $27.1M of BNB debt against BTCB and USDT collateral at a 1.16 health factor. This borrower is effectively short BNB, so May's 15% rally compressed its health factor rather than easing it, the one large position the rally made riskier and the clearest directional name in the book. Even here a forced unwind would not hit the market in one block, since the 50% close factor and competing liquidators clear it in pieces against BTCB and BNB, two of the deepest markets on the chain.

4. Transaction Volume

Total volume for the month (excluding the May 9 artifact):

| Type | Volume | Share |

|---|---|---|

| Repay | $1.86B | 37.6% |

| Borrow | $1.83B | 36.9% |

| Withdraw | $0.64B | 12.8% |

| Supply | $0.63B | 12.7% |

Clean monthly volume was $4.95B, with a median day near $20M. Borrow and repay together were about three-quarters of activity. The two busiest days were May 13 (about $2.0B of matched USDT borrow and repay) and the end-of-month BNB rally days. As noted in Section 1, the May 9 BNB and Cake spike was a self-netting flash-loan artifact and is excluded throughout.

Volume by market (clean):

| Market | Volume | Share |

|---|---|---|

| USDT | $2.87B | 58.0% |

| BNB | $1.42B | 28.7% |

| BTCB | $0.38B | 7.7% |

| ETH | $0.16B | 3.2% |

| USDC | $0.06B | 1.2% |

USDT dominates flow at $2.87B, reflecting its role as the primary borrowed stablecoin, followed by BNB at $1.42B as borrowers adjusted positions around the rally.

5. Collateral Structure & Revenue

Top collateral/borrow pairs:

| Collateral | Borrowed | Debt | Apr Debt | MoM | Users |

|---|---|---|---|---|---|

| SolvBTC | BTCB | $51.3M | $52M | -1% | 22 |

| BTCB | USDT | $48.0M | $48M | 0% | 2,174 |

| asBNB | BNB | $40.9M | $37M | +11% | 37 |

| xSolvBTC | BTCB | $36.5M | $42M | -13% | 13 |

| BTCB | BNB | $32.0M | $34M | -6% | 1,877 |

| SolvBTC | USDT | $31.4M | $34M | -8% | 23 |

| BTCB | BTCB | $23.6M | $25M | -6% | 601 |

April pair debt is reported to the nearest $M, so MoM percentages are approximate.

Two structurally different borrowing populations coexist. The correlated E-mode strategies are large and concentrated: SolvBTC and xSolvBTC collateral backing BTCB debt ($51.3M across 22 users and $36.5M across 13 users respectively) are BTC-on-BTC leverage loops with minimal directional risk, as is the $23.6M BTCB-against-BTCB self-borrow. The asBNB-against-BNB pair ($40.9M, 37 users) is the BNB-side equivalent. Against these sit the broad retail pairs, where thousands of users borrow stablecoins or BNB against BTCB (2,174 users on BTCB/USDT, 1,877 on BTCB/BNB). These are the genuinely directional positions and the ones that drove most of the month's liquidations.

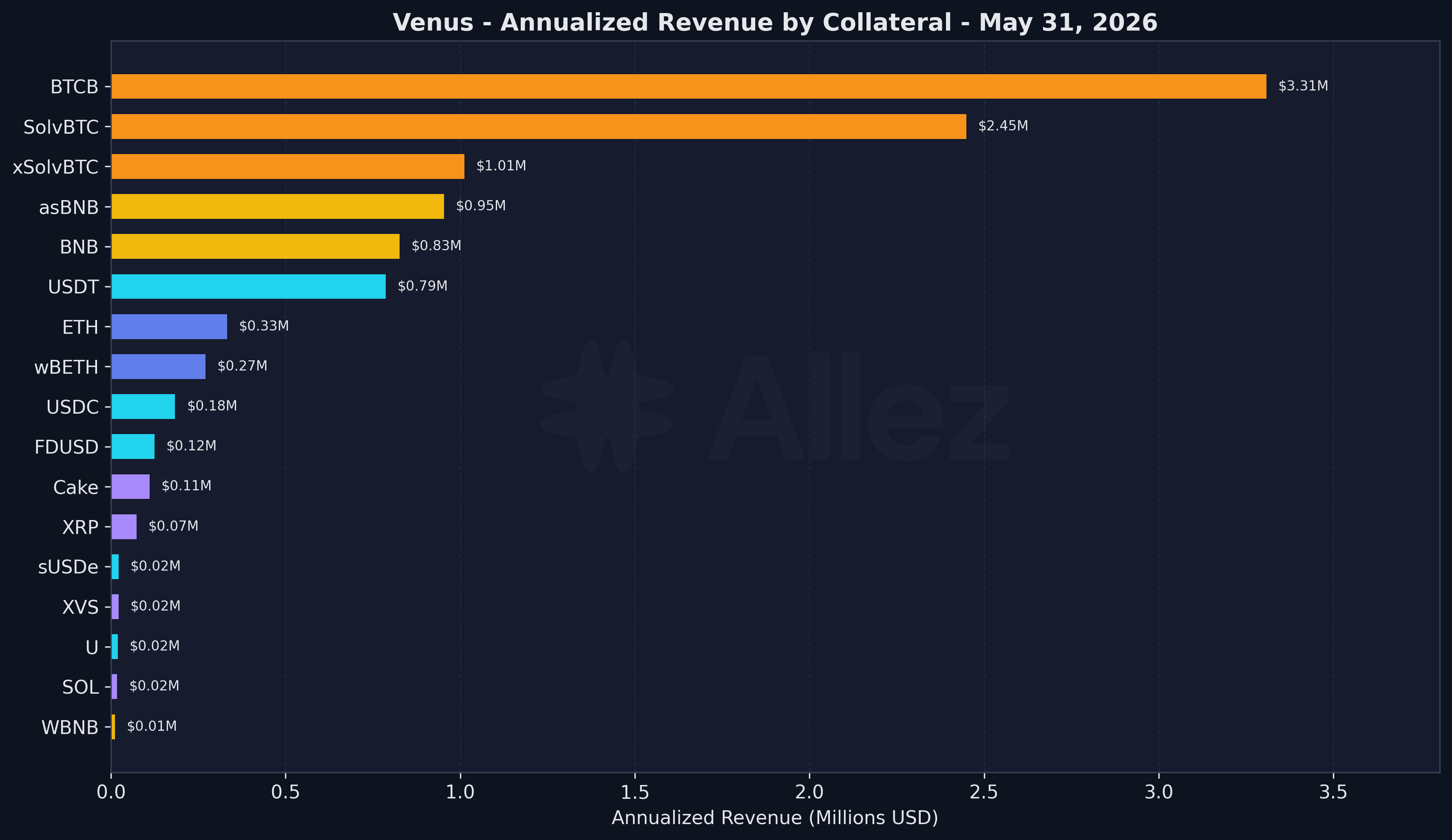

Annualized revenue by collateral:

| Collateral | Supported Debt | Annual Revenue | MoM |

|---|---|---|---|

| BTCB | $131.7M | $3.31M | -8% |

| SolvBTC | $95.0M | $2.45M | 0% |

| xSolvBTC | $36.7M | $1.01M | -5% |

| asBNB | $55.1M | $0.95M | +7% |

| BNB | $29.3M | $0.83M | +5% |

| USDT | $37.7M | $0.79M | +1% |

| ETH | $13.9M | $0.33M | n/a |

Annualized collateral-attributed revenue totals $10.5M across the protocol, down 5% from April. The BTC complex (BTCB, SolvBTC, xSolvBTC) supplies over $6.7M, more than 60% of it. The table lists the top collateral types as an annualized run-rate on current debt and rates.

Realized revenue by market (May):

The figures below are what the protocol actually accrued during May, measured from on-chain interest events. They are grouped by borrowed market, where interest accrues, rather than by collateral.

| Market (borrowed) | Gross Interest | Reserve Factor | Protocol Revenue |

|---|---|---|---|

| BTCB | $146K | 30% | $43.9K |

| USDT | $394K | 10% | $39.4K |

| BNB | $84K | 30% | $25.1K |

| USDC | $99K | 10% | $9.9K |

| ETH | $44K | 20% | $8.7K |

| FDUSD | $60K | 10% | $6.0K |

| U | $35K | 10% | $3.5K |

| Others | $29K | mixed | $5.2K |

| Total | $891K | 16% | $142K |

Borrowers paid $891K of gross interest in May, of which the protocol retained $142K as reserves at a 16% blended reserve factor. The $891K realized is in line with the $10.5M annualized run-rate above (about $875K per month). BTCB is the single largest revenue source despite USDT generating more gross interest, because the BTCB market carries a 30% reserve factor against USDT's 10%.

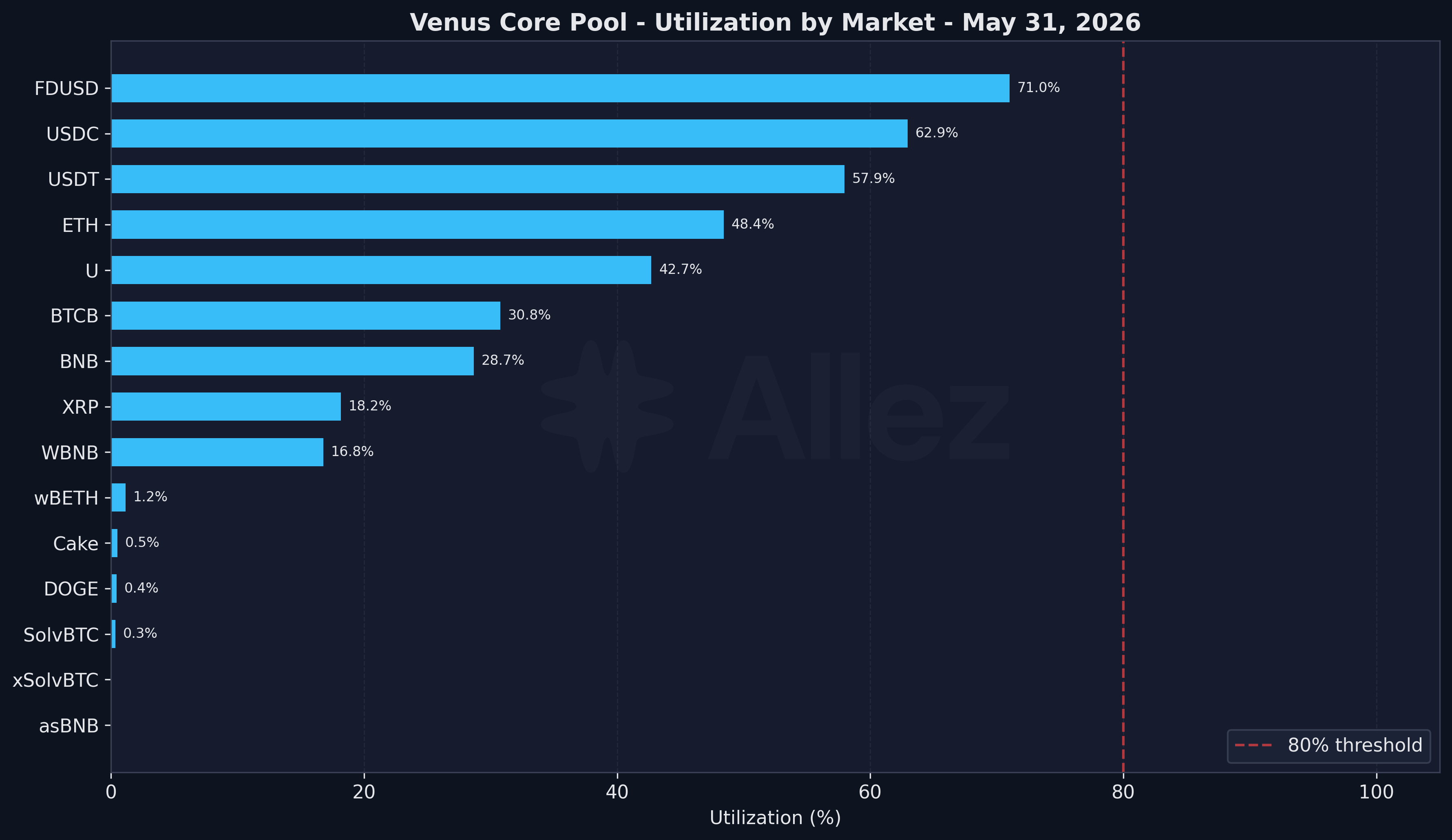

6. Utilization

Utilization is moderate across the board, with no market near a stress level. The highest are FDUSD at 71.0%, USDC at 62.9%, and USDT at 57.9%, all comfortably below the 80% threshold. The notable change is ETH, where utilization fell from 88.3% at the end of April to 48.4%. ETH debt fell 51% ($39.9M to $19.5M) while supply held in token terms, consistent with large ETH borrowing positions opened in April being unwound.

7. Conclusions & Forward Look

May reduced risk on net while BNB rallied 15.3%. ETH was the standout, with debt halved and utilization down from 88.3% to 48.4% as large April positions unwound. Liquidations stayed minimal ($447.5K, no cascade), and directional Critical-tier debt fell to $10.9M. The dollar declines in supply (-2.1%) and debt (-5.2%) were mostly BTCB and USDC outflows outweighing the BNB mark-up, not a change in user behavior. On governance it was a cleanup month: DAI off-boarded, vSXP retired, and TUSD and FIL wound down, alongside two risk-infrastructure additions, the tighten-only EBrake Executor and the Oracle Dynamic Protection Mode, a deviation-bounded price guard on the borrow path.

Things to watch in June:

-

wBETH and ETH stablecoin debt. The $4.3M of stablecoin debt against wBETH sits within 10% of liquidation, and ETH has been the weakest major collateral. A further ETH decline is the most likely source of new liquidations.

-

USDC contraction. Supply fell 31.7% in one month, and if it continues it would thin USDC liquidity and is worth confirming against any external migration.

-

Borrower concentration. The top three borrowers hold $117M (28% of protocol debt). Most run correlated E-mode structures, but the third-largest ($27M of BNB borrowed against BTCB and USDT, health factor 1.16) carries genuine directional exposure and is the main single name to watch.

Venus Core Pool enters June stable. Two live risks remain: a renewed ETH drawdown would catch the wBETH and ETH stablecoin loans already near liquidation, and continued BNB strength would pressure the one large short-BNB borrower at a 1.16 health factor. Everything else is correlated leverage that liquidates against itself.

Appendix: Asset Category Classification

| Category | Assets | Supply | Debt |

|---|---|---|---|

| BNB | BNB, WBNB, asBNB, slisBNB, PT-clisBNB | $567M | $128M |

| BTC | BTCB, SolvBTC, xSolvBTC | $633M | $122M |

| Stablecoins | USDT, USDC, FDUSD, DAI, U, USD1, TUSD, sUSDe, USDe | $306M | $176M |

| ETH | ETH, wBETH, BETH | $61M | $20M |

| Altcoins | Cake, XRP, ADA, LTC, LINK, DOGE, others | $56M | $2M |

Correlated positions hold collateral and debt in the same price category (for example SolvBTC against BTCB, or asBNB against BNB) and carry low directional risk. Uncorrelated positions span categories (for example BTCB against USDT) and carry true directional exposure.

Scope: Venus Core Pool on BNB Chain only. Isolated pools and non-BNB deployments are out of scope for this report.

This report represents independent risk analysis by Allez Labs for the Venus Protocol community.

Prepared by: Allez Labs Risk Team

Report Date: May 31, 2026

Next Report: June 2026 Monthly Report published in July 2026